RESEARCH

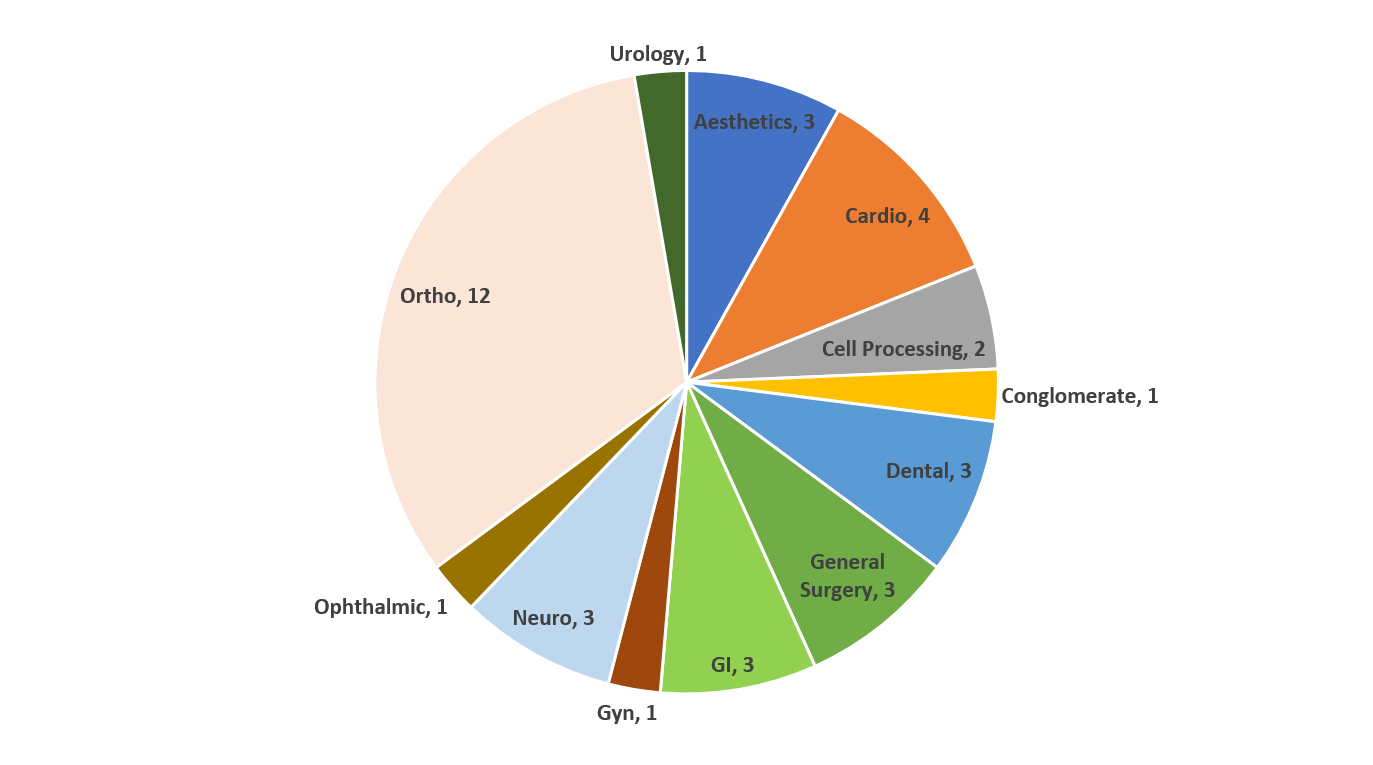

Medtech M&A is continuing at a brisk pace well into 2017, as we report some trends in the 37 deals announced so far this year. Notably, 12 of 37 announced transactions, or 32%, were in orthopedics. The remainder of the deals were distributed relatively evenly between sectors, as depicted below:

Unsurprisingly, the biggest transaction announced in 2017 is the proposed acquisition of C.R. Bard by Becton Dickinson for $24B, or about 6x revenues. More remarkable is evidence of the increased interest in the Aesthetics space, growth in which has been attributed in part to more consumer awareness and acceptance as well as increased adoption of these treatments and services among men. There have been three transactions announced in the Aesthetics space this year, including Allergan’s $2.5B acquisition of Zeltiq and Hologic’s $1.7B acquisition of Cynosure, which happen to be the second- and third-highest-value deals of the year. Neuro was also an active space, with three transactions announced, the most significant being Integra LifeScience’s planned acquisition of J&J’s Codman Neurosurgery business for $1.1B.

J&J/Ethicon completed a rare transaction in its purchase of Torax Medical. Torax describes itself as developing and manufacturing minimally invasive treatments for digestive, incontinence and obesity disorders, and their lead product is the Linx System for the management of gastroesophageal reflux disease. The terms of the transaction were not announced.

Among orthopedics companies, Stryker remains an active acquirer, having recently announced its $700 million bid for Novadaq, which offers real-time perfusion imaging intraoperatively. With their clear commitment to growth via M&A and more than $3.6B in cash on their balance sheet, we expect Stryker to continue their acquisitive strategy, particularly in the general surgery space, where they’ve been most active of late. We also note a number of spine companies (Interventional Spine, Spinal Elements, Medyssey) among the dozen transactions in orthopedics announced so far in 2017.

These acquisitions are consistent with what we have observed about medtech M&A in the past: acquisitions are executed largely by strategic acquirers, the industry leaders who prioritize novel technologies that can enhance their current offering and that they can integrate into their established commercial organizations. The recent volume of activity – and at strong valuations – provides evidence of the long-term growth and innovation in medtech.

Posted: August 15, 2017