INNOVAHEALTH ANNOUNCEMENTS

Today we’re looking back on medical technology private placements and exits in 2018 and are happy to report a highly active year. In the surgical and therapeutic device space, we identified 112 private placements valued at more than $1.4 billion; on the M&A front, we can report 67 transactions in this segment, with the publicly disclosed total transaction value at approximately $15 billion.

Highlights and Takeaways

Private Placements

- Mean and median transaction size was $12.4 and $5.3 million, respectively.

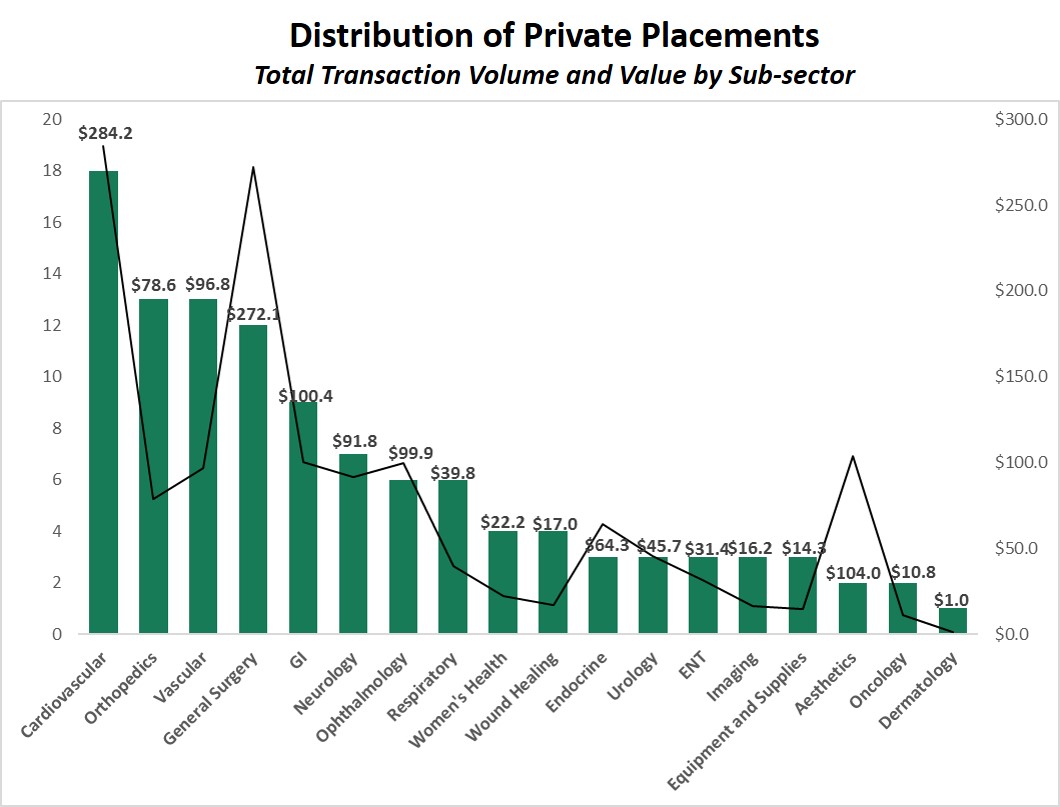

- Cardio led the sector in terms of number of transactions (18), followed by orthopedics (13 transactions), vascular (13 transactions) and general surgery (11 transactions). Transaction values were similarly distributed across sub-sectors, with more than $284 million invested in cardio, $78.6 in orthopedics and $96.8 million in vascular. The complete distribution of transaction count and total value by sub-sector is represented below.

- The largest deal of the year in our space was a $220 million round for Auris Health, the developer of a 510(k)-cleared robotics technology used in bronchoscopic procedures. The round was led by Partner Fund Management, who were joined by new investors Wellington Management, D1 Capital Partners and Senator Investment Group and existing investors including Mithril Capital, Lux Capital and Viking Global.

- Other large rounds included $97 million for breast implant company GC Aesthetics, $58 million for Beta Bionics, which is developing an autonomous bionic pancreas, and approximately $60 million for Stimwave, the developer of a pain management device.

M&A

- Mean and median transaction size was $416.4 and $155.0 million, respectively.

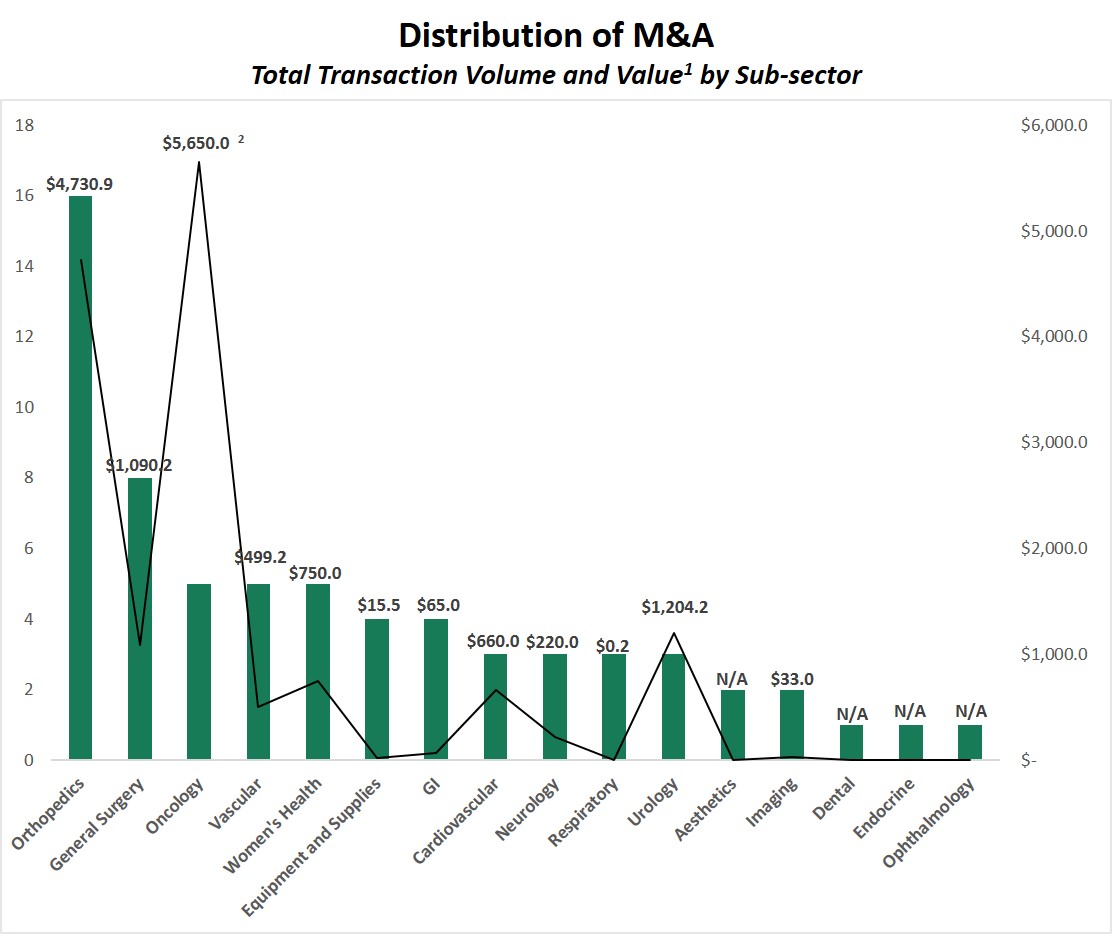

- Orthopedics led the medical device segment in terms of transaction volume, with 16 transactions valued at a total of $4.7 billion (approximately a third of the total disclosed transaction value for the year). Two of the largest transactions of the year were in orthopedics as well, namely the Medtronic Acquisition of Mazor Robotics and Stryker’s acquisition of K2M.

- Other active sub-sectors included general surgery (8 transactions) and oncology, vascular and women’s health, which each had 5 transactions. The complete distribution of transaction count and total value by sub-sector is represented below.

1 Value is based on publicly disclosed transaction valuations.

2 Valuation amount represents Boston Scientific/BTG announced transaction.

- Boston Scientific was the most active acquirer of the year, logging nine transactions valued at more than $1.4 billion (though not all valuations were publicly disclosed). Stryker announced three transactions (Invuity, HyperBranch Medical and K2M), and JNJ announced two (Emerging Implant Technologies and Orthotaxy).

- We also note the high premiums acquirers paid for innovation. While the mean and median transaction valuations were a healthy 6.5x and 4.3x revenues, respectively, valuations for companies with novel technologies were significantly higher. For example, Medtronic’s acquisition of Mazor Robotics, a surgical planning and guidance platform used in spine procedures, was valued at 28.3x revenues; Wright Medical’s acquisition of Cartiva, which holds a PMA for its cartilage-like polymer technology, was valued at 12.4x revenues; and Boston Scientific’s acquisition of Augmenix, which markets a hydrogel spacer to protect against adverse events associated with prostate cancer radiotherapy, was valued at approximately 12.0x revenues.

Medical technology had a busy year, with substantial funding flowing into innovative companies that will eventually become targets for M&A. The strategic acquirers in our space have demonstrated a strong appetite to grow by acquisition, and they maintain the cash balances to continue to execute deals at this pace. We’re looking forward to what 2019 will bring.

Source: Pitchbook.

Posted: January 22, 2019